YouTube DELETES CoinDesk's Entire Channel

YouTube DELETES CoinDesk's Entire Channel

This is exactly why decentralization is the future.

Full Stack

YouTube Bans CoinDesk

Last night I noticed (h/t Jason Nelson) that the show I co-host on CoinDesk, “The Hash”, had been taken offline.

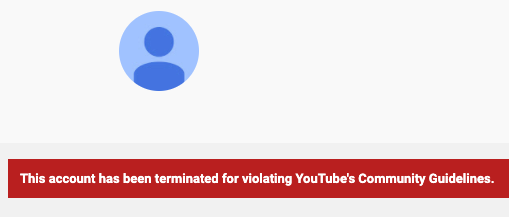

In fact, YouTube had deleted CoinDesk’s entire channel:

Just like that, the video channel of one of the most popular crypto news sites is deleted from existence.

YouTube wrote in an email to CoinDesk:

"Content that encourages illegal activities or incites users to violate YouTube's guidelines is not allowed on YouTube."

They didn’t elaborate further. What illegal activity they’re referring to, I have no idea.

On February 8th of this year, CoinDesk launched CoinDesk TV, with daily offerings like “The Hash” that I’m part of, which focuses on crypto and culture.

Luckily, CoinDesk wasn’t relying on YouTube for an audience — they have actually been promoting people watch the show directly from the new CoinDesk.tv website. It seems with good reason, as relying entirely on a 3rd party to host your content is clearly a big risk.

Many crypto YouTubers have learnt this lesson the hard way over the past few years, with YouTube purging channels in large swaths. The mass deplatforming has extended well beyond crypto of late, with well-known personalities like biohacker Josiah Zaynor also being booted. The mainstream is starting to understand the risks of relying on large centralized companies, who get to dictate the content on their platform. Both Josiah and Tim now host their channels on Odysee, a decentralized video platform that provides creators with an alternative — and the videos here can’t be taken down, because it’s built on the decentralized LBRY protocol.

If large companies continue to exercise, with an increasingly heavy hand, their right to censor and delete communities on their platforms, it wouldn’t be surprising if our decentralized future arrives sooner than we’d thought.

You can subscribe to my Odysee channel here.

Quick Bytes

Coinbase is Bringing The Entire Ecosystem Into a Brave New World

“The current financial system is rife with high fees, unequal access, and barriers to innovation,” Coinbase CEO Brian Armstrong insisted in a letter to the SEC and potential investors. “If the world economy ran on a common set of standards that could not be manipulated by any company or country, the world would be a more fair and free place, and human progress would accelerate.”

His words are tucked inside of the Form S-1 filing required by the US Securities and Exchange Commission (SEC) of any company planning on going public. Late last year, Coinbase revealed its intentions to do just that via a direct listing on Nasdaq, skipping a traditional Initial Public Offering (IPO) altogether, but this latest disclosure (a prospectus) gives real details and a few Easter Eggs.

For example, since its founding summer of 2012, the premiere US cryptocurrency exchange has processed nearly half a trillion, yes trillion, in trading. Life got so good less than a decade later, Coinbase in 2020 took-in profits of $322 million, a 140% jump from the year prior.

The company lists no fixed headquarters, defining itself as a full remote outfit. Evidently, the pandemic forced Coinbase to pivot in this regard, so that by May of 2020 such overhead was eliminated.

The filing also contained a nod to the Satoshi Nakamoto genesis address of the first 50 bitcoin issued on January 3, 2009: 1A1zP1eP5QGefi2DMPTfTL5SLmv7DivfNa.

Analysts like Lex Sokolin, of The Fintech Blueprint, recently upped his valuation of the exchange from $15 billion to as much as a whopping $100 billion. His modeling of the company is compelling.

“The last quarter generated $600 million in revenue,” Sokolin calculated, “which was as much as the first three quarters combined. So we think 2020YE was somewhere around the $1.2+ billion range, and the company is annualizing at over $2 billion.”

“The price of the core crypto assets doubled, doubled, and then doubled again,” he continued. “When BTC is at $60,000 and ETH is at $2,000, Coinbase has a symmetrically large increase in its core business. Reminder that in July, BTC was at $7,000. As a result, cumulative trading volumes jumped to $450 billion from $200 billion.”

Sokolin is particularly bullish by legacy money continuing to flood into crypto, with Coinbase poised to take advantage as its ”institutional custody and prime brokerage business has become 50% of their $90 billion under custody.”

For veterans of the space infused with a cypherpunk ethos, there’s a sense of both chest-swelling pride and sheer terror at the prospect of Coinbase going mainstream. An onboarding superstar company supported by the community as a nice way to introduce mom and pop to decentralized money … might just become a significant point of failure.

Inevitably, the company’s concerns will turn toward more traditional public companies’ concerns. Already there are rumblings from Coinbase about foreign competitors who aren’t regulated by the SEC. Why should Coinbase be held in check when others aren’t? This almost surely isn’t going to end with the deregulation of the industry, but instead with the long arm of US law extending even further. Not good.

On the other hand, the exchange is a mostly trusted (!) unicorn within the ecosystem, and it might not be too optimistic to believe that if one company had to ascend to such levels, Coinbase is a good choice. They might soon be in a better position to guide coming regulation, perhaps making it less odious.

US Treasury Secretary Calls Bitcoin “Extremely Inefficient”

“I don’t think that bitcoin … is widely used as a transaction mechanism,” Treasury Secretary Janet Yellen explained to CNBC during a recent New York Times DealBook conference. “To the extent it is used I fear it’s often for illicit finance. It’s an extremely inefficient way of conducting transactions, and the amount of energy that’s consumed in processing those transactions is staggering.” Cryptobeat has wondered aloud what pretexts the new administration will employ to intervene in Bitcoin, and it does appear those are becoming clearer if the last line is any indication.

Speaking of Inefficient

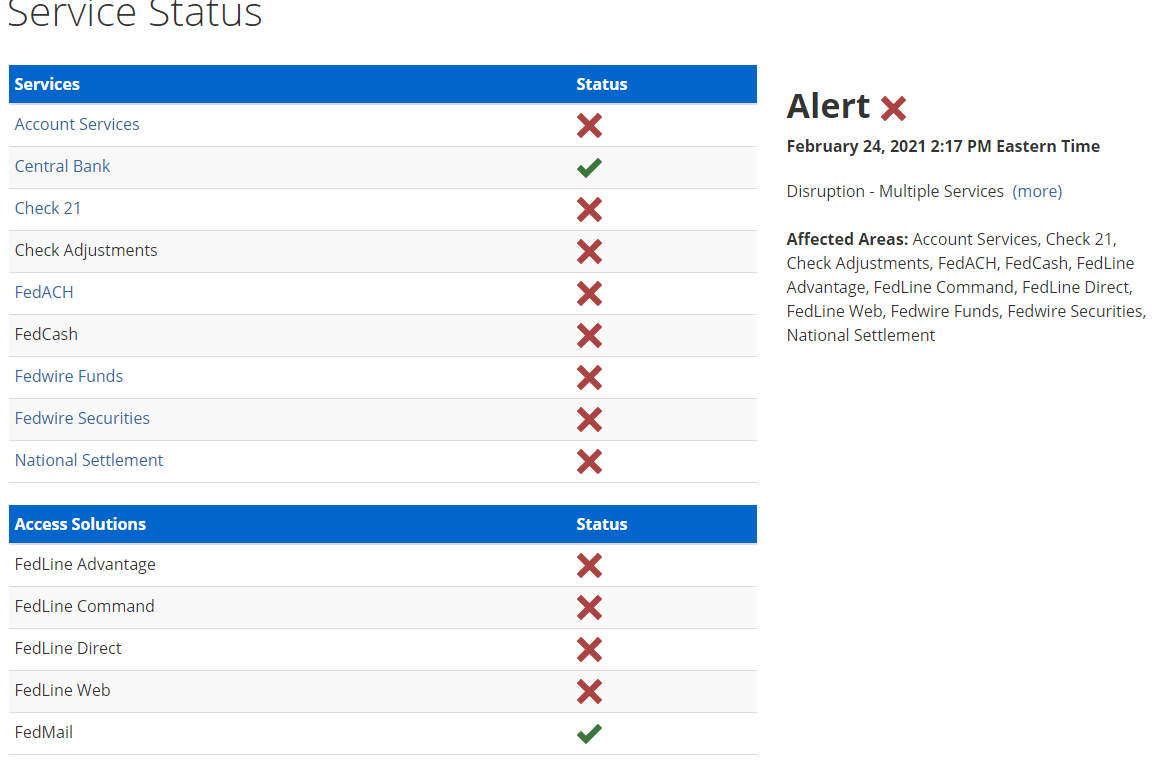

On Wednesday, February 24th, 2021, the US central bank noted what The Wall Street Journal (WSJ) termed “an unspecified error,” disrupting key economic services performed by The Federal Reserve such as ACH, Check 21, FedCash, Fedwire, and national settlement “for several hours.”

The WSJ elaborated, “Central-bank officials couldn’t immediately recall a similar episode affecting its systems, which had been seen as extremely reliable. They allow the Fed, which is known primarily for setting interest rates, to perform its less-public role of acting as a bank for the nation’s banks and for the U.S. government. It handles tasks including collecting checks, electronically transferring funds, and selling and redeeming Treasury bills—services that were all offline for more than three hours on Wednesday.” A cyberattack has been ruled out.

Tether, Bitfinex Reach Settlement With New York AG

The world’s most popular stablecoin, and continual source of debate and controversy, recently settled a lingering lawsuit with the state of New York. “After 2.5 years and 2.5M pages of info shared,” Tether noted, exasperated, “we admit to no wrongdoing and will pay US$18.5M to resolve this matter.”

Importantly for the company’s reputation, they also insisted, “no finding that Tether ever issued without backing or to impact crypto prices. This settlement shows our commitment to the future of the industry, and to transparency with quarterly disclosures of @tether_to reserves going forward.”

By contrast and in a parallel universe, New York Attorney General Letitia James, who prosecuted the case, responded to the settlement: “We're ending @bitfinex and @Tether_to's virtual currency trading in New York after the companies covered up about $850 million in losses around the globe and deceived the market by overstating reserves. Those trading virtual currencies in New York cannot avoid our laws, period.”

Erik Voorhees diligently pointed out another potential hazard to the NYAG:

Cryptocurrency Has Become Elon’s World

It’s official. We now await every utterance from the founder of Tesla. Every meme. Every hint. Every clue. Even his profile emoji makes news and moves markets. Elon Musk engaged online for weeks in Doge, of course, the space’s inside joke that eventually posted no-joke gains on Musk’s mere notice, apparently. Rumors are furious that the SEC has taken notice and might soon come knocking on Musk’s door as a result. The richest man in the world did more than shrug the SEC off. He welcomed them.

Beeple NFT Sells for $6.6 Million in ETH

We have to be honest. We’re still trying to get comfortable with the world of NFTs. Gemini’s Nifty Gateway is putting up a pretty good fight. Their latest announcement involves the artist @Beeple and the piece, CROSSROAD. “The #1/1 from beeple's first NG drop has just resold on the secondary market for $6.6 million. History has just been made.”

By C. Edward Kelso, NBTV contributor, and Naomi Brockwell, NBTV host.

Find more of Kelso’s work here: @coinfugazi / coinfugazi.com

Why not even mention Hive and 3speak that is building a decentralized video storage system?