May 2021’s China-Induced Bloodbath

May 2021’s China-Induced Bloodbath

Cryptocurrency Miners Scramble to Adapt in a Fast-Changing Environment

Cryptocurrency Miners Scramble to Adapt in a Fast-Changing Environment

A statement from one of the precious few people who iron-hand steer a country with more than a billion souls helped crash cryptocurrency markets this month.

While chairing the 51st meeting of the State Council Financial Stability and Development Committee, an exclusive government body in the Chinese Communist Party, the lowest-ranking Vice-Premier, Liu He, decreed, “Stability should be a top priority for the financial system,” ensuring “reasonable, adequate liquidity, prevent and defuse risks, and create a virtuous circle of the economy and financial sector.”

The 4th Vice-Premier took special aim at financial risks, which he stressed “should be prevented and controlled resolutely,” including renewed government efforts to “combat mining and trading of bitcoin.”

It was enough to slash Bitcoin prices by half and rather quickly, dragging with at least the top 200 alternate coins down as well.

Miners and pools, like HashCow and BTC.TOP “halted all or part of their China operations,” according to Reuters. “Cryptocurrency exchange Huobi on Monday suspended both crypto-mining and some trading services to new clients from mainland China, adding it will instead focus on overseas businesses.”

Some kind of China ban is almost a well-worn punchline at this point for veteran enthusiasts, most famously due to the country’s ratcheting up restrictions back in 2017, outlawing crypto exchanges and ICOs.

Elaine Yu and Chong Koh Ping of The Wall Street Journal explained:

“China is trying to rein in cryptocurrency activities even as the country has embraced the technology underlying bitcoin and has plans to roll out its own digital yuan that will be controlled by its central bank. Beijing also wants to shut down cryptocurrency-mining activities because they consume massive amounts of electricity, often from coal-fired power plants, while the country pledged to manage its carbon emissions.”

The move came after “three Chinese self-regulatory groups issued a similar notice and said financial institutions need to increase their monitoring activities and terminate and report virtual-currency-related transactions that violate the country’s laws,” The Journal reported. “The trio—the National Internet Finance Association of China, the China Banking Association, and the Payment & Clearing Association of China—also warned of sanctions for firms that didn’t comply.”

That days-earlier statement, under the country’s central bank banner, can be read here.

Crypto Twitter pundit Dovey Wan added perspective:

“EVERY PAST CYCLE, one significant China bans caused material impact and major collateral damage. We had that in 2013 and 2017, and moon so hard afterwards. The impact weakens each single time until it’s completely obsolete. Basically China is opting out of the crypto game, short sighted and so desperately. Authoritarianism is always opposite of freedom, and the faster it’s out of the equation the better. I’m so bullish for what we are heading into, seriously.”

Chinese journalist known as Wu Blockchain tempered the supposed-ban’s actual implementation. Noting “the first enforcement measures have just been officially introduced and come from Inner Mongolia,” Wu found, “Beijing seems to allow local governments to issue policies on their own. This may not be bad news.”

Wu also gave a glimpse into how resilient Chinese miners are adapting to new realities. “BTCM, a Chinese company listed on the Nasdaq, announced an investment of 9.33m to build a mine in Kazakhstan with 100 MW. It also cooperates with another Kazakhstan mine to host the mining machine, which is 60 MW. At present, Chinese miners are seeking overseas mines. Kazakhstan was the most active Bitcoin mining location outside of North America last year, with many Chinese miners. Kazakhstan already has 6% to 10% of Bitcoin's entire network hashrate.”

Bitcoin Mining Council

American investor and recent Bitcoin convert Michael Saylor, no doubt spooked by China and subsequent market moves, announced his hosting of “a meeting between @elonmusk & the leading Bitcoin miners in North America. The miners have agreed to form the Bitcoin Mining Council to promote energy usage transparency & accelerate sustainability initiatives worldwide.”

In order to help meet environmental, social, and governance (ESG) goals, Saylor brought together Musk and leading industry executives from “@ArgoBlockchain, @blockcap, @Core_Scientific, @GalaxyDigitalHQ, @HiveBlockchain, @hut8mining, @MarathonDH & @RiotBlockchain” in order “establish an organization to standardize energy reporting” and “ educate+grow the marketplace.”

Musk described the meeting as “Potentially promising.”

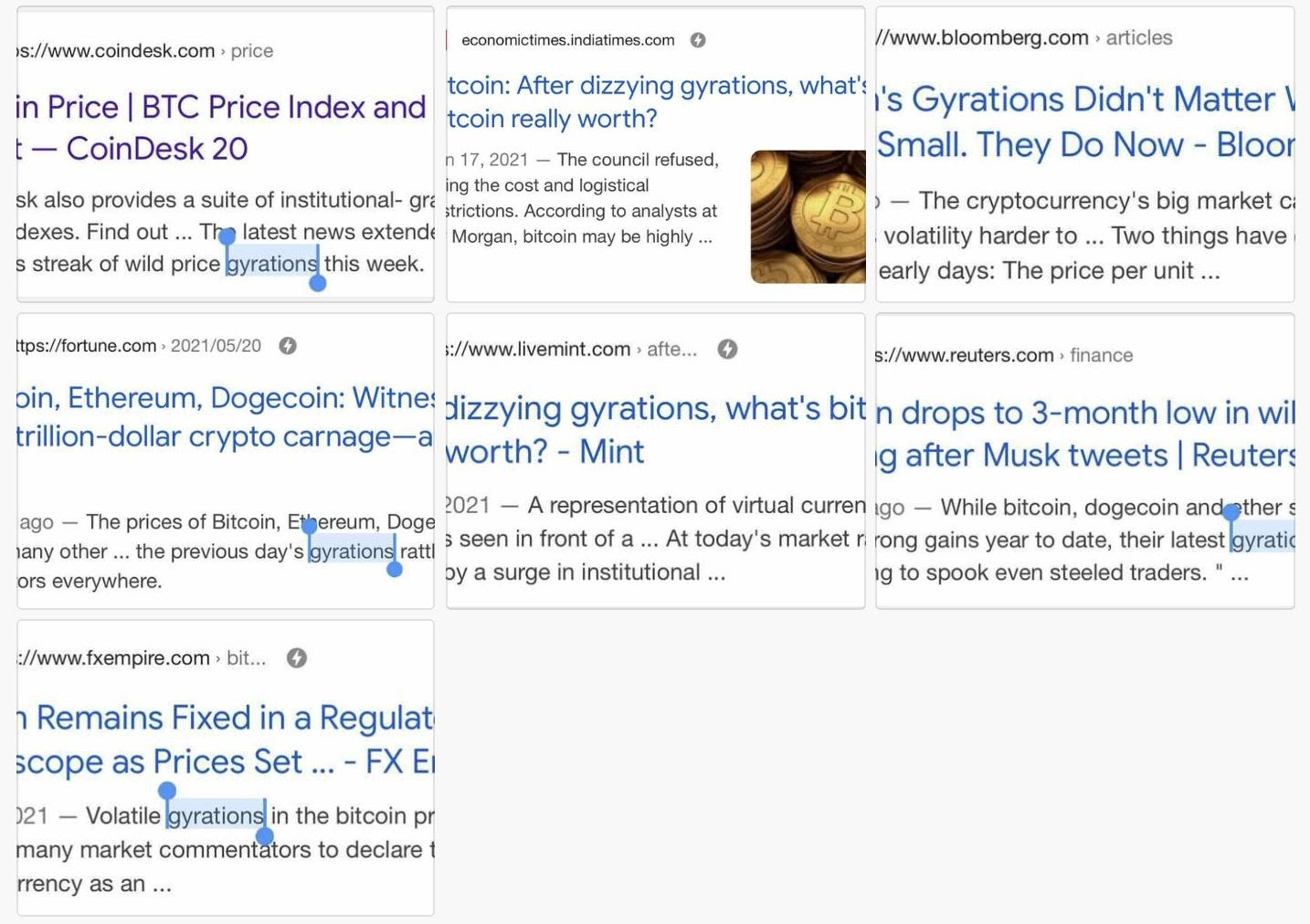

Go Ahead, Tell Him

Kraken CEO Jesse Powell recognized a suspicious amount of unanimity among the corporate press in documenting recent crypto market downturns. And while much of financial media is insanely incestuous and mind-numbingly lazy, they’re doubly more so when it comes to cryptocurrency news. Seizing upon the odd use of the word “gyrations,” Powell found more than a half dozen pieces with that rare phrasing, back-to-back this week. “Tell me this isn't coordinated,” Powell posted snidely.

Coinbase Gulps at the Coming DEX Onslaught

Already unnerved by the cryptocurrency phenomenon, mainstream finance got a nice look into the abyss that is its future. Journalist Alexander Osipovich and photographer Victor Llorente profiled Hayden Adams of decentralized exchange (DEX) Uniswap. They contrast Adams and DEXes generally as upstarts to the recent Wall Street crypto darling Coinbase, already considered something of an established incumbent.

“Last month,” Osipovich explained, “$122 billion in transactions took place on DEXes, as they are known, up from less than $1 billion a year earlier.” And though it is “unclear how much of a threat DEXes pose to centralized exchanges,” Coinbase has “taken note.” So much so, “Coinbase listed competition from decentralized platforms as a potential business risk before going public last month.”

Africa Number Go Up!

Documenting Bitcoin cheered, “Africa is leading the world in peer-to-peer #bitcoin trading volume growth, with 22% in the last three months. Citing metrics from UsefulTulips, it shows how OTC trading in places like Sub-Saharan Africa is nearly pacing that of North America, according to numbers gathered from LocalBitcoins and Paxful.

Huskers Go Digital

The US heartland is jumping on the crypto trail, albeit in more conventional ways. CoinDesk reported this week, “Nebraska’s unicameral state legislature has passed a bill that would create a state bank charter for digital asset depository institutions.” Following precedent set by Wyoming with Avanti, “Bill 649 would create a charter that would give consumers and institutions places to custody their digital assets,” allowing “already existing state-chartered banks in Nebraska to open crypto banking divisions.”

By C. Edward Kelso, NBTV Head Writer.

Subscribe to the Cryptobeat newsletter and receive it directly in your inbox each week!

NBTV runs entirely on donations. Would you like to send a (US) tax deductible donation? Visit our Cointree page!